Will Jio dominate the Indian tech industry for the years to come?

If so, then how can it become India's Tencent

This post was originally written in August/September 2020 and hence, might have some backdated information.

Recently at work, we took a step back from the news cycle around Jio and staged a debate discussing whether it would dominate the Indian tech industry 10 years down the line.

While I was arguing in support of Jio, my opponent was highlighting the flaws.

I documented our findings and have shared a few takeaways from this vibrant discussion. Hope you guys enjoy it.

Reliance: A debt-free, first of its kind digital infrastructure company

While Jio has managed to become debt-free on paper, there is still a long arduous task at hand of delivering on the promised vision with less than net ~$10 billion in hand. Here are a few hurdles Jio still faces:

Still an oil-to-chemical company

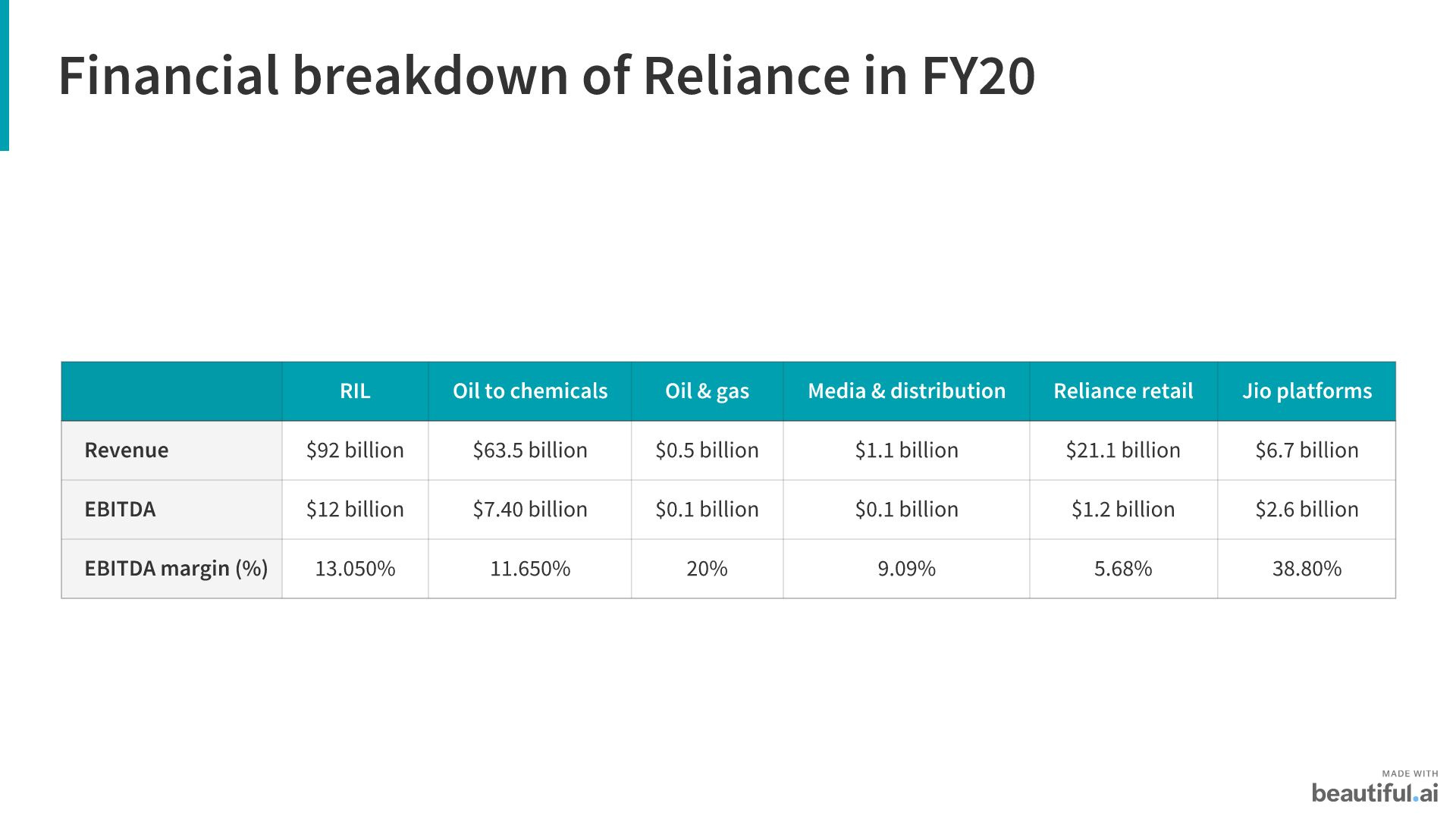

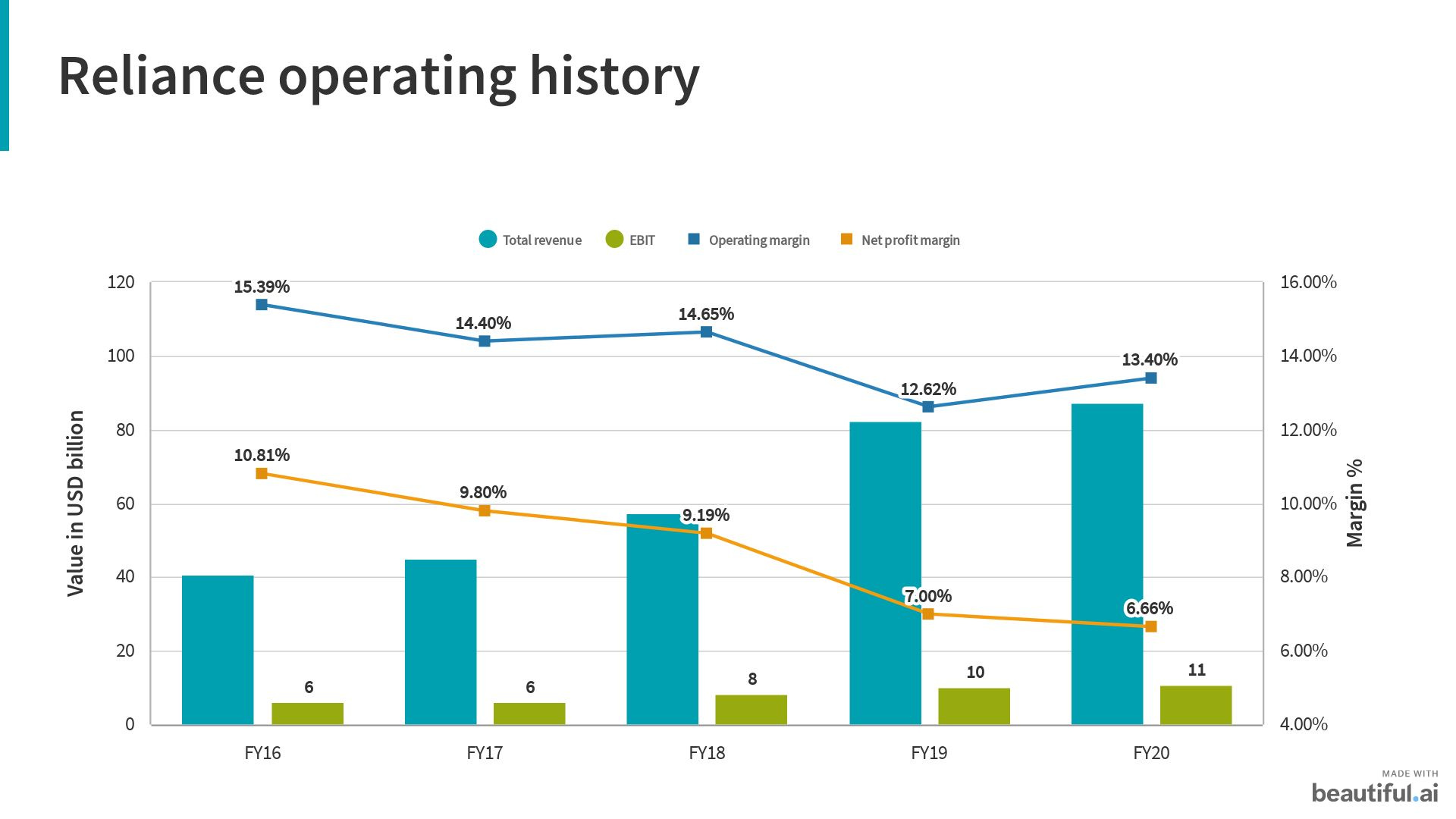

RIL amassed $92 billion in revenue in FY20. Only 10% came from digital services + media & entertainment. So, while Ambani is telling investors how obsessed Reliance is with being a consumer-focused tech company, it’s still very much a work-in-progress.

Rapid expansion and exponential growth

Reliance’s consumer businesses have delivered hyper-growth with 49% EBITDA growth, contribute about 20% of consolidated EBITDA.

5 years ago, all their EBITDA was from oil and materials. Since then, their consumer and technology businesses have achieved massive scale with exponential growth.

It will be interesting to see how this revenue split donut evolves.

Debt, cash flow, and valuation

In the past 3 months, Jio has raised an astronomical sum in equity, close to $20.6 billion for ~33% stake, to doctor its current debt situation, coming at a time when interest rates are quite low. Investors include the likes of Facebook, Google, Microsoft, Qualcomm, and other marquee private equity investors. Including other rights issued to stakeholders, fundraise stands at $28 billion.

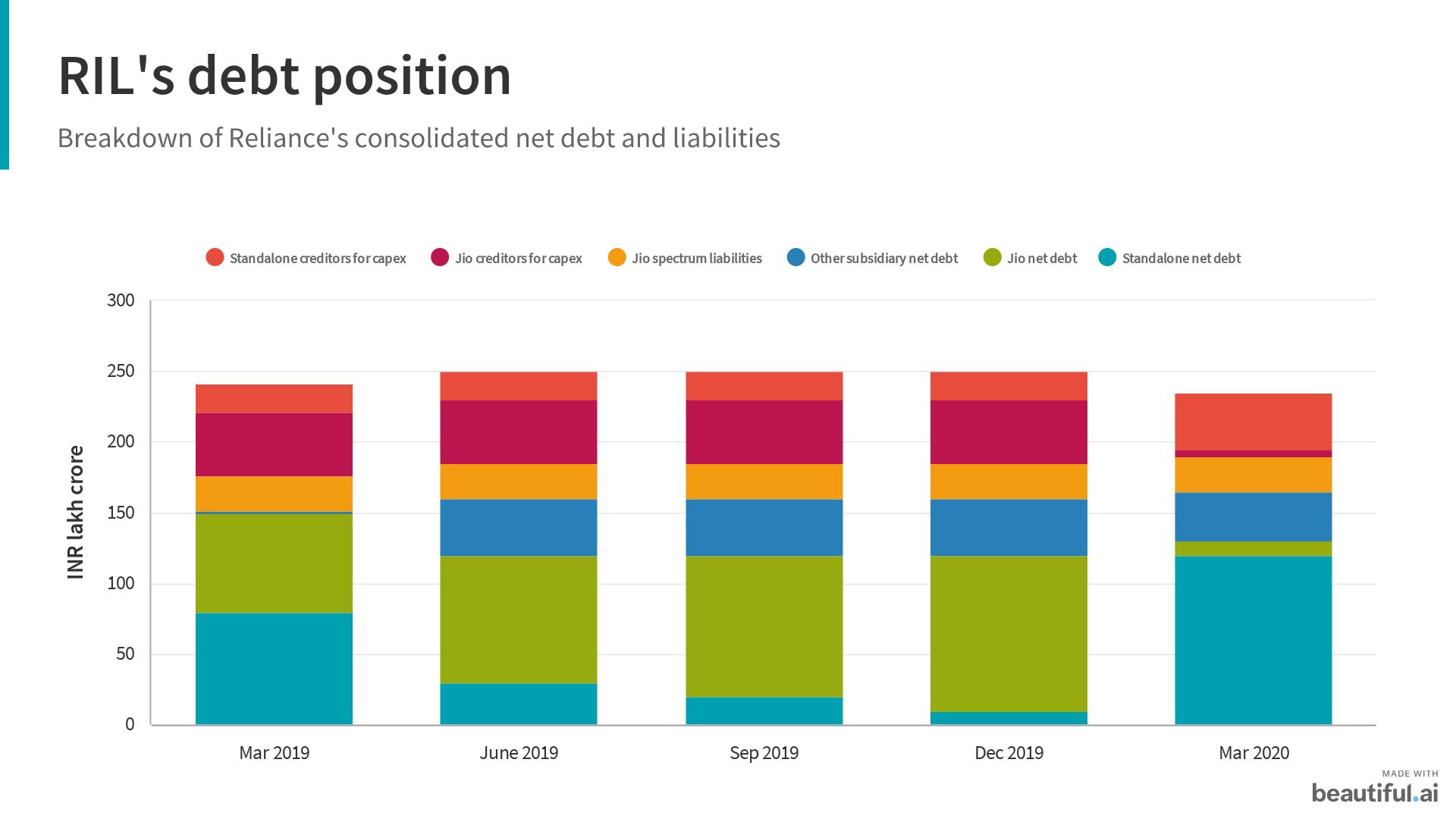

And how does Reliance’s debt compare to its free cash flow? Reliance’s consolidated net debt stood at $23.5 billion. Jio spent $30 billion building India’s first 4G network and bankrupting competitors with low-ball pricing. In terms of cash flow, RIL made a net of $2.83 billion cash equivalent in FY19, and analysts estimate the free cash flow to remain steady at $2-$2.5 billion in FY21. The cash flow to debt ratio, at 10%, is a little low, leaving Reliance with little money to pursue its ambitious goals.

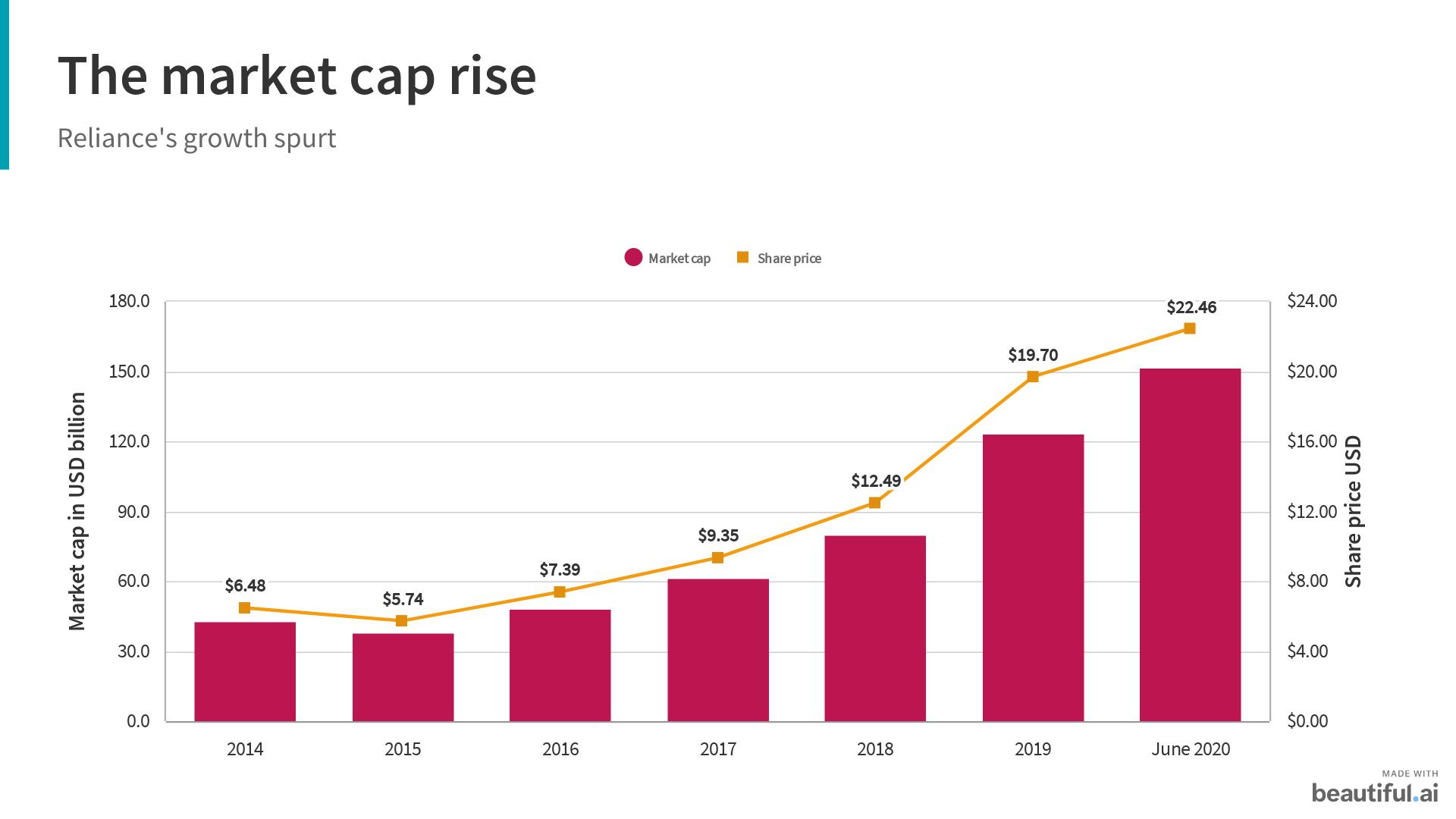

Given the company’s cushy position on the net debt front, RIL shares have reached new record highs and its market cap has crossed $150 billion, becoming the first Indian company to reach this milestone. RIL may not exactly be a debt-free company, but the debt overhang has lifted from over its stock.

Valuation is fundamentally about the future cash flow and NOT the revenue

Reliance had argued that Jio should not be seen as merely a telecom business but as a technology business, competing with the likes of Google and Facebook.

One way for a company to have huge cash flows is to capture more value/share of the wallet across the chain. It not only helps the unit economics but also translates into a sustainable competitive advantage.

Having said that, I’m still dubious about valuing Jio as a technology company cause it remains to be seen how effectively it can monetize the various platforms and apps. Thus far, the most tangible piece of technology Reliance has produced isJio Glass.

The $70 billion valuation tag for Jio Platforms comes at ~23X EV to EBITDA (vs 10X for Airtel). To justify these numbers, Jio would have to quickly monetize other parts of its value chains and generate cash flows.

Based on an internal analysis, we ended up with an EV of $60-$65 billion for the oil to chemical business, retail at $35-$40 billion, and telecom at $55-$60 billion.

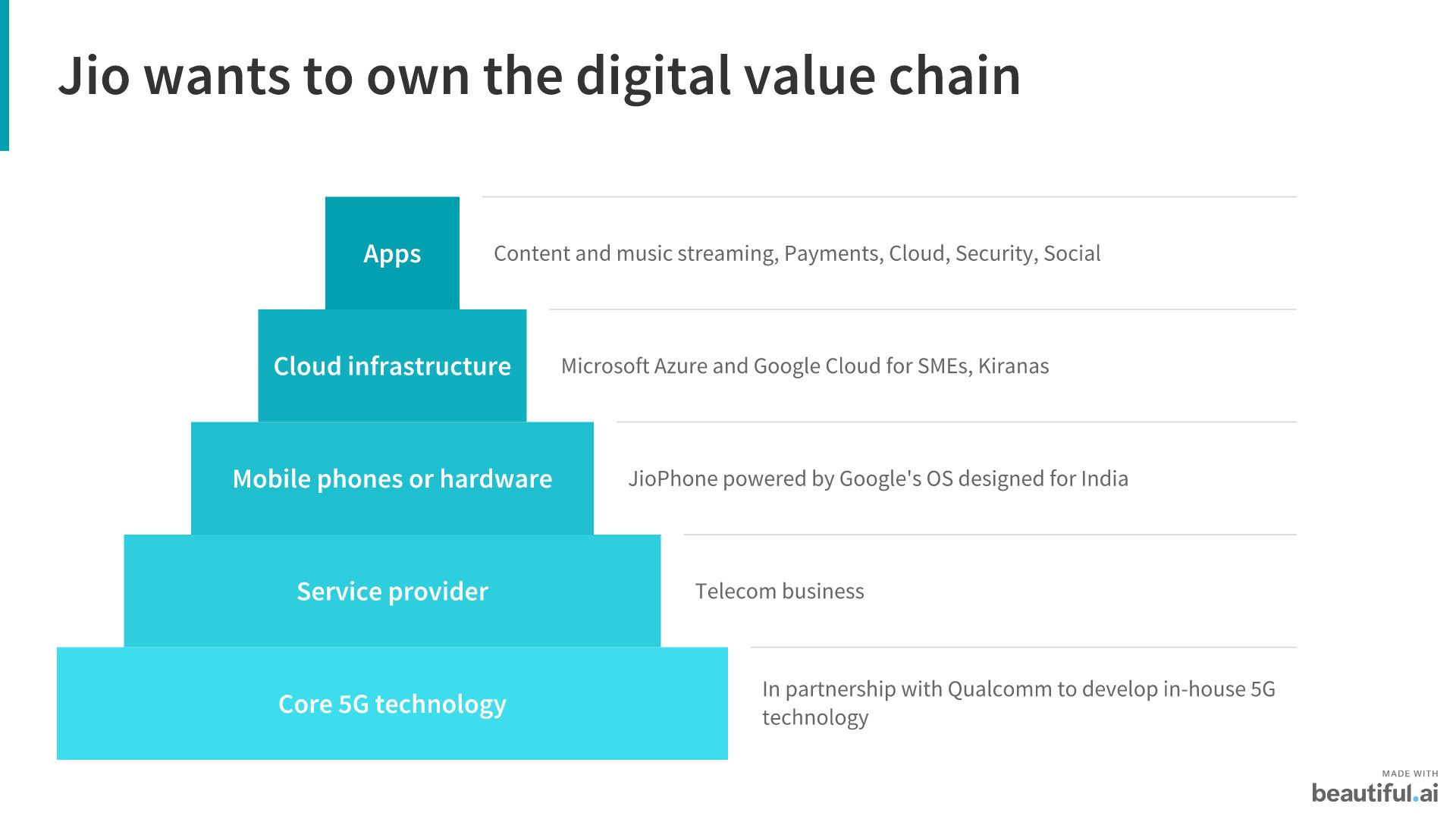

Digital infrastructure

Moving up the stack from fixed-cost infrastructure to high-margin services

Typically, any business that Reliance enters, it intends to own the value chain. Take its oil business — starting with polyester yarns, it gradually secured the supply chain expanding into petrochemicals, then refining, and finally oil & gas exploration.

Given the aggressive consumer land grab that we’ve witnessed in India in the past 5 years, it’s hard not to notice what Reliance has done to sell Jio as a digital giant to investors. With homegrown 5G tech, it could charge a tax like AWS.

To be fair, the fact that each layer of the pyramid is an economic ocean to uncover gives Jio an opportunity but many of these are winners take most kind of market, hence it’s doubtful if it’ll still land in a place with growing revenues and healthy cash flow, justifying a humongous valuation. Some might say that many of these are winner takes most markets and RIL will find it tough to make a mark.

Some of this money raised by Jio could be used for the development of 5G tech.

Jio’s $20 billion investment in a full IP network makes it easy to set up a 5G network when compared with other Indian telcos with legacy networks.

An ability to set up its own system translates into a competitive advantage.

This is because networks are complicated, high-investment, and low-margin business. Jio can develop its 5G network and put it in the cloud, and sell it to other telcos.

How will Jio develop 5G equipment?

These plans to develop 5G tech would be in keeping with the Qualcomm partnership. Reliance also acquired Radisys, a US-based firm, in 2018 for $67 million to help with developing telecom equipment. This equipment will be designed in India and either built-in abroad or India.

But a standalone 5G network isn’t here yet — and won’t be a reality until at least 2025 (except in China, where one operator plans to launch the world’s first standalone 5G network next year). Till then, Jio will upgrade existing 4G core infrastructure with 5G tech so that it supports new 5G frequency.

It’s an audacious plan fueled by an obvious reluctance to let Huawei, accused of being an apparatus of the Chinese state, be planted in the fast-speed internet networks that will run everything from power stations to autonomous cars, dealing with sensitive data.

But making your equipment is just one piece of the puzzle. Reliance also needs deep pockets for the 5G spectrum. The 5G spectrum band is between 3,300 - 3,600 MHz with 1 MHz costing ~$70 million, and operators requiring a minimum of 100 MHz — a $7 billion capital investment just for acquiring spectrum rights.

The fact of the matter is, we’ve seen very few examples of operators that have successfully built their systems. Vietnam is the only country with a state-owned operator that aims to construct a 5G network based on its software and hardware.

Lastly, a pertinent question is how useful is 5G really to consumers? In my mind, 5G is good for self-driving cars, IoT, and other enterprise applications. Do consumers really need 5G?

Jio’s own UPI

In China, Alibaba and Tencent have built native digital currency infrastructures. Reliance is considering building its own proprietary payments system, just like UPI. With little information available on this development, one can only say that it sounds like an interesting proposition but might be far-fetched.

Jio is a platform, and unlike aggregators, you succeed (or fail) in the aggregate

With a platform approach, Reliance is laying a strong foundation to play a key role across a user’s digital life and digital journey of tech companies. None of the operators we can think of globally promises to build, offer, and control what Jio is capable of. With products like JioMeet, it is building low-cost infrastructure for the masses.

Jio needs to build a symbiotic relationship with these product developers building on top of Jio’s infrastructure by aligning incentives.

JioMeet could be India’s virtual classroom and possibly more

As pointed out above, platforms act as an interface between two modularized pieces of a value chain — users and developers building on top of a platform, offering diversity and competition, to set the flywheel in motion. Attracting (and maybe acquiring) startups like OutSchool for India will potentially attract more startups/developers to the platform to build Edtech and Healthcare (telemedicine) businesses. The end goal is to make JioMeet a platform that takes advantage of different modularized pieces of the value chain and enable different businesses to be built on top of it.

Investment options for Reliance with a significant cash position

Traditionally, Reliance has deployed a high debt, high cash strategy. This helps in keeping its investment options open. Having seen multiple triggers in recent times — raising ~$28 billion, increase in omnichannel retail, increase in ARPU in the telecom business — Reliance expects to cut net debt in half by end of FY21, and once the remaining asset monetization comes to a realization, net debt could be zero. But it may well retain a large sum of the cash from asset sales rather than repay all its creditors.

So what are the different investments Reliance can make with the significant cash position of $5-$8 billion post debt realization?

Reduce other liabilities on the balance sheet such as deferred payments and provisions, totaling over $7 billion.

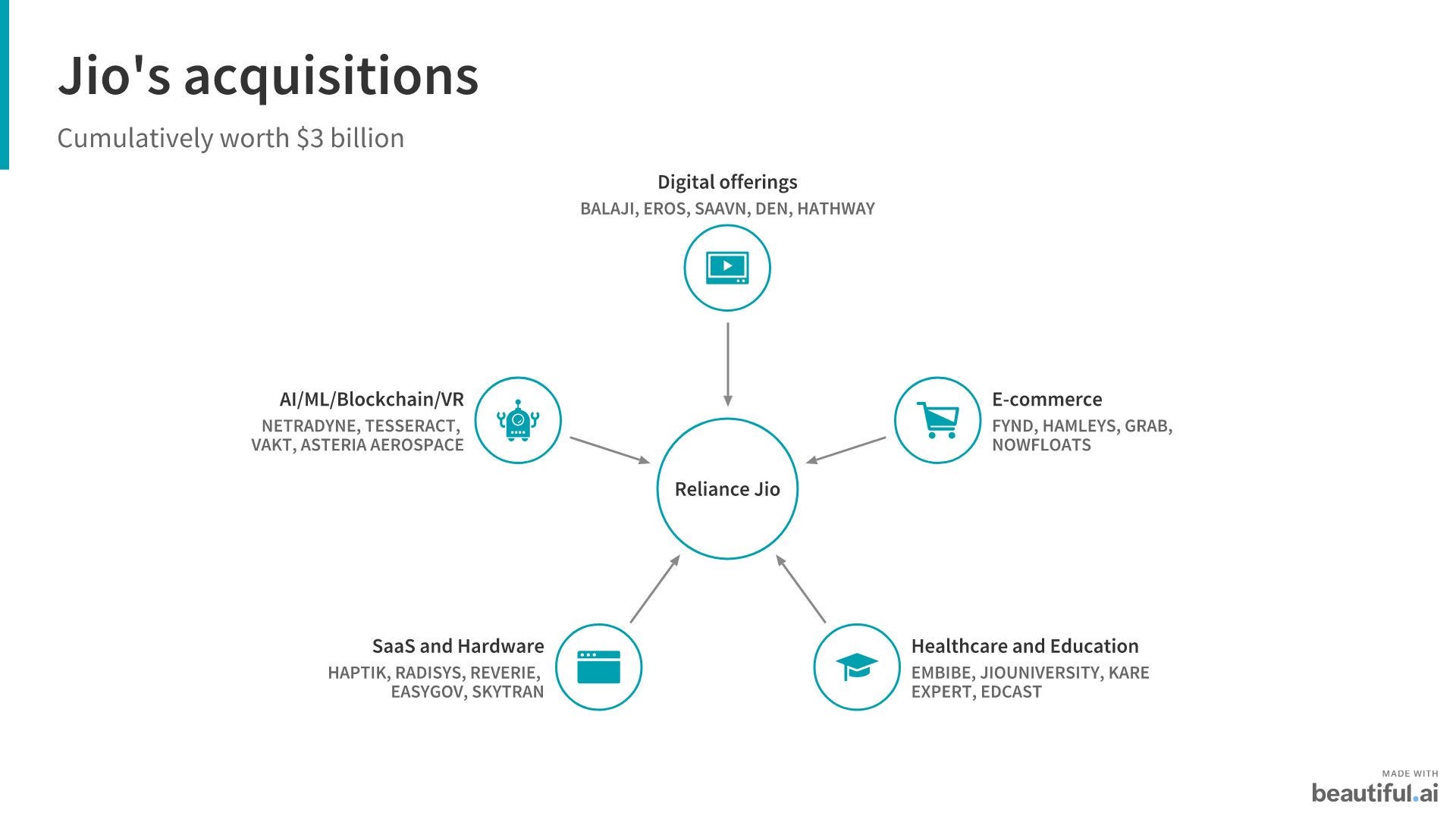

More investments in M&A, especially in the Internet and retail sectors. [Reliance has made acquisitions worth $3 billion to date — this is expected to increase in the next few years].

Investing in homegrown 5G solution and spectrum ($7 billion for spectrum and humongous costs for standalone network).

Consider safe and liquid investment options like short-term debt funds, taking a bet on the interest-rate cycle.

An important thing to note — the fundraising spree has been unprecedented, but 75% of the proceeds from the rights issue will be received in FY22. The issue was structured such that investors needed to pay only 25% of the value of the shares they applied for, with the rest expected in two installments in FY22.

Ergo, all investments mentioned above will be phased, 5G upgrade being a priority.

Retail and JioMart

In all our discussions, one thing we all agreed to is that the biggest opportunity that Reliance wants to pursue is Retail. And why not? It’s $700 billion, ~25% of the GDP. It’s a business that is relatively easy to enter but difficult to sustain.

So a battlefield is set for startups operating in B2B (Udaan, ShopKirana, JumboTail, etc) or B2C retail space, and it’s only going to get fiercer with Reliance akin to become the master negotiator. In a low-margin business such as this, dominated by physical retailers of all shapes and sizes, we expect a lot of consolidation in the near future.

But for manufacturers like HUL, who survive on the fact that the retail supply chain is fragmented and democratized, will feel threatened to lose their bargaining power if there is a master negotiator.

Whatsapp will drive commerce

An immediate cash flow generating stream that Jio plans to unlock using WhatsApp’s distribution is through JioMart. In his bid to compete in e-commerce against likes of Amazon and Flipkart, Ambani has partnered to leverage the popularity of mom-and-pop stores. Jio’s strategy to disrupt without disrupting (by going B2B2C) and digitizing these shops with supply, logistics, payments, and inventory tracking does 4 things:

Bind them in an economic value sharing concord — being an online aggregator and providing other services.

Being vertically integrated into this value chain with Reliance Retail.

Create a market for selling cloud services to small and medium scale enterprises.

Keeping in mind its partnership with Microsoft, Reliance will be looking to capitalize on the untapped market of digitizing small and medium scale enterprises.Open doors for working capital financing and micro-loans.

Coronavirus has accelerated the pace of digital adoption and by connecting to JioMart, a virtual store, neighborhood Kirana shops can outgrow their limited shelf space. Again, what works in the favor for Jio over here is the vertical integration it has — Reliance Retail will be sourcing supply to these Kirana shops and fulfilling orders in some cases. For JioMart to be successful, it needed a partner that has deep penetration cutting across income segments and do the distribution online. India’s love for WhatsApp is well documented with 400 million MAUs.

JioMart might already be a unicorn

With 400K orders/day, assuming an AOV of $7 (INR 500), JioMart looks on course to ~$1 billion in GMV. In comparison, Bigbasket Daily delivers around 250-300K orders/day, and Grofers and Amazon Pantry do ~100K orders/day. JioMart has 13.5K Kirana shops on its platform and targets 30K by end of the festive season.

With a meager 5% operating margin, it means $50 million operating profit. Taking benchmark valuation multiples from this space, I believe we might be looking at the fastest unicorn in the world. Sweet deal indeed.

The future of retail

Reliance Retail runs supermarkets and is India’s largest consumer electronics chain, the cash-based wholesale stores have fast-fashion, and are integrated with JioMart. It has 12,000 stores in 7,000 towns and reported $22 billion in revenue in FY20.

Reliance recently closed its acquisition of Future Group’s retail assets for $3.5 billion to bolster its position in India’s retail segment. As part of the deal, Reliance will inherit fashion and grocery retail from the listed entities such as Big Bazaar, FoodHall, FBB, Central, Heritage Foods, Brand Factory, barring apparel brands Lee Cooper, etc. with over 1,700 stores. Reliance Retail network also works as a distributor for Jio connectivity services. With 28.7 million sq. ft operating area, including Jio stores, Future group acquisition will add 23.6 million sq. ft, significantly strengthening its footprint and physical outreach.

Data businesses are better-off by a mile

Data is the new oil: Mukesh Ambani

In its journey to get 400 million subscribers, JioPhone was instrumental in acquiring users and expanding the ambit of data consuming customers. Since its launch, JioPhone has sold over 70 million units. Jio single-handedly created a compelling need for Indians, who had never owned a phone before, to consume large amounts of data. It did so by creating an ecosystem of services custom-made for these users — from online chatting, video, and music streaming to digital payments, to cloud services — it became Spotify, Apple, Netflix, Verizon, Dropbox (all in one). Result: In 2019, Jio carried 70% of all 4G traffic and 61% of overall data traffic. Now the JioPhone is about to get an upgrade — an optimized AndroidOS software, tailor-made for India, by Google.

The partnership with Google and Facebook will open monetization channels for Reliance in ads and analytics, sitting on top of all this data with little to no effect.

Lending opportunity

Telcos are de-facto banks because of the distinct distribution advantages.

It’s a trend playing all over: from Indonesia, Vietnam, Myanmar, Colombia, and Africa, telcos have found a sweet spot in banking and financial services.

With JioPhone, JioMart, and as for most of Jio’s offerings, one thing’s clear — it wants to unlock the power of the masses. With UPI, GST combined with Google and Facebook, and its own subscriber data, Jio has access to data that can provide superior insights into consumer and supplier habits than the traditional financiers. The underwriting models will be backed by data that can underwrite on-demand, unsecured loans, and serve the 500 million largely underserved users in India-4 (lower middle class, household income < $500 per month).

These users (the reason for the existence of a startup like Meesho), are typically ignored by the traditional banking and finance institutions, and avail loans off of informal credit lenders charging up to 100% interest rates on credit. This represents a $300 billion credit opportunity. The 500 million includes business owners and families for underwriting working capital and personal loans.

Tech leadership and product expertise

Does Jio have the capacity to offer products with a delightful user experience?

Let’s be honest, tech is not Reliance’s forte and that’s a tough one considering it’s pitching a tech firm to investors. In the name of global, best in class products, we have JioMeet and JioChat that are blatant, pixel by pixel copies of category-defining apps (Zoom and WhatsApp respectively). Take Reliance Digital and Fresh too — both were marketed as tech-first offerings but ended up offering a buggy customer experience. And with JioGlass, Reliance will be competing with Apple and Google directly — unparalleled brands with amazing products.

Reliance can harbor in-house tech talent by acqui-hiring visionary tech leaders with strong credentials in execution, trickling change at an organizational level.

Jio can compensate for that through a well-thought acquisition strategy

Given tech is not its forte, how can Reliance trigger growth in the high-margin products and services segments? Inorganically through acquisitions seems like a very viable option. With an ambition to further disrupt the consumer space (telecom and retail) through the use of tech, Reliance seems to have over-purchased into diversification (investing $560 million in media and education, $200 million in retail, and $100 million in digital), achieving below-par results.

How have these acquisitions performed? Even with a list of companies under its belt, Reliance failed to model it to scale and succeed as it did with Jio. Acquisitions like JioSaavn and Embibe have performed underwhelmingly, to say the least.

Acquisitions can help it strengthen in terms of capabilities, reach, and adoption by acquiring companies that give it an advantage by being synergistic. For instance, acquiring a company like Delhivery would mean it’s not only grabbing a slice of the pie off of other eCommerce players, it’s also forwardly integrating itself into its retail and consumer-facing businesses by becoming a last-mile player itself.

At a glance, not a lot of these acquisitions make sense. But dig deeper and you’ll realize that Reliance was always trying to pursue the digital value chain, one piece at a time. Reliance wanted to own carriage, content, and commerce. Looking through this lens, these acquisitions start to make much more sense. All these partnerships and acquisitions are only an extension of Motabhai’s ambitions.

Why are players like Amazon, Facebook, Google, Microsoft, Qualcomm interested and what do they bring to the table?

Instead of seeking to usurp companies like Facebook or Google that already have a major market share in India, Jio is partnering with them.

Jio has the right partners by its side — it gained access to 400 million, ever-engaged WhatsApp users, just like that. Imagine the hard work and time spent by Paytm in getting those 350 million users over 10 years and now Jio comes along, brokering the right partnerships to strengthen its bid. It must be frustrating to some end.

Facebook brings distribution and payments, Microsoft brings cloud, Google brings software and product expertise, and Qualcomm brings 5G layer. The idea is simple, rather than toying with regulatory hurdles themselves, partner with a powerful, expansionist, and monopolistic force in India to take a slice of the pie back to the US.

The political and financial muscle in times of license raj

Many commentators would point to Jio practically being in the bed with the government (and the regulators). Reliance’s proximity and connections to the Indian government are so well documented that the Facebook partnership is being seen as political risk insurance. Bending rules and providing walkovers does suggest that the Indian government considers it mutually benefitting — by letting Reliance attract investments, build infrastructure and in turn, create the market. These investments have helped build the infrastructure that the state couldn't build, and other corporates found daunting.

India can take cues out of the Chinese playbook — an economic policy that aligns itself with the expansion of a few large capitalists is more manageable and produces faster results than one that has to play referee to free and open competition.

Although, questions will remain on the creation of anti-competitive market structures.

Seeds of doubt

Five reservations leap to mind on Jio and this whole spectacle.

First — the cost of servicing equity is far more expensive than debt and has a dilution impact on existing shareholders. So wouldn’t it make sense to raise new debt when it has liquidity and interest rates are low? On the contrary, so are the risks of failure coupled with long payback periods for generating operating cash flows.

Second — there is an aggressive push from Reliance to bifurcate its oil to chemical, retail, and digital business, but it may still get burdened with a permanent discount as a holding company with assets spread across digital, retail, and organic compounds.

Third — Ambani wants to emulate several successful Chinese firms, all at once — but I’m in two minds if India is ready in terms of physical infrastructure or balance sheet.

Fourth — monopolies have a deadweight loss; Startups will have to share the economic value and monopolistic rules can lead to capturing disproportionate value. Then again, if an efficient market means that majority of cash flows to Valley or China, should we particularly care about efficiency?

Fifth — no such business models discussed above have shown to work globally. No tech leader in any one of these layers worldwide has succeeded in migration to even 2 or 3 other stacks to date. Amazon failed with its Fire Phone and Fire OS; Verizon failed with Yahoo. The closest to owning more than one layer is Apple (iPhone, iOS, iTunes) and Amazon (retail, Kindle, and Firestick). Hence, if this works, it will create a competitive moat that will be insurmountable.

Remember — more companies die of indigestion rather than starvation.

In conclusion

Indians left a wave of desktop computing behind them when they took up mobile phones and Ambani powered them with cheap Internet. As for Reliance, it still has to demonstrate that one company can be India’s answer to everything, from Zoom and Tencent to Huawei and Xiaomi, while also being a Verizon. India is a mix of characteristics combining those from emerging and developed markets both. The businesses it currently plans to enter are monetizable only when India Inc’s balance sheet is more supportive.

Public equity investors primarily look for 3 things in stock on the market: growth, cash flow, and risk (not in that order necessarily). While debt on the balance sheet is considered a sign of growth, Jio has been trying to get rid of it. For an ordinary mortal looking to invest, this is no more than a pure PE play in the publicly traded markets — not as a risk-free investment it is being made out to be.

The timing here is also interesting, given recent tensions with China, and India's dependence on China.

Reliance knows how to expand massively in a short time — Jio and JioMart are prime examples. And this is where I believe it will continue to be strong and build a big business (in retail and telecom). What about the rest? Only time will tell.

Superb writeup.

Reliance is a juggernaut. It cannot be stopped because of simple and deadly equation of :

1. A very highly ambitious entrepreneur.

2. So far a well and shrewdly crafted strategy of developing and owning the value chain. Even you have stated that it wants to own and dominate content, carrier and commerce.

3. A really extremely efficient businessman to manage different political landscape in India having an experience and expertise (running down to 3rd generation) of dealing and managing with two most powerful political outfits simultaneously.

4. Why RIL went to debt reduction is because it is the flavour of the season - both, domestically as well as globally. Every one knows that the cost of equity is much higher than the cost of debt, but, still the world over, over the last 3 to 4 years, suddenly there is a great rush to give unprecedented valuation to low/zero debt companies.

5. Finally, all three SBUs/listed subsidiaries, namely, O2C, Retail and Telecom will be managed independently by three scions of RIL boss and therefore it makes sense to carve 3 niches.