Solving the employability problem in India

Why B2B(2C) model might be more suited than B2C to employ grey-collar India

The pandemic has provided an unprecedented acceleration to Edtech, behaving like the demonetization moment, resulting in an astronomical rise in the number of users, naturally improved engagement time, and an enhanced willingness to pay.

This is because schools do not have the tech infrastructure to tutor remotely, all coaching centers are shut-down, and besides electronic presentations, there isn’t much tech readiness for teaching, assessment, and evaluation at school and university level.

But what we also saw unfolding during the pandemic was the long looming learning crisis compound into an employability crisis, that has forced us to take a step back and rethink the way we want to prepare our population for a career. For a challenge as big as poverty in magnitude, we brainstormed solutions that can not only help achieve the desired learning outcomes but also operate in a model that might be better suited to build a meaningful and sustainable business at scale.

Background

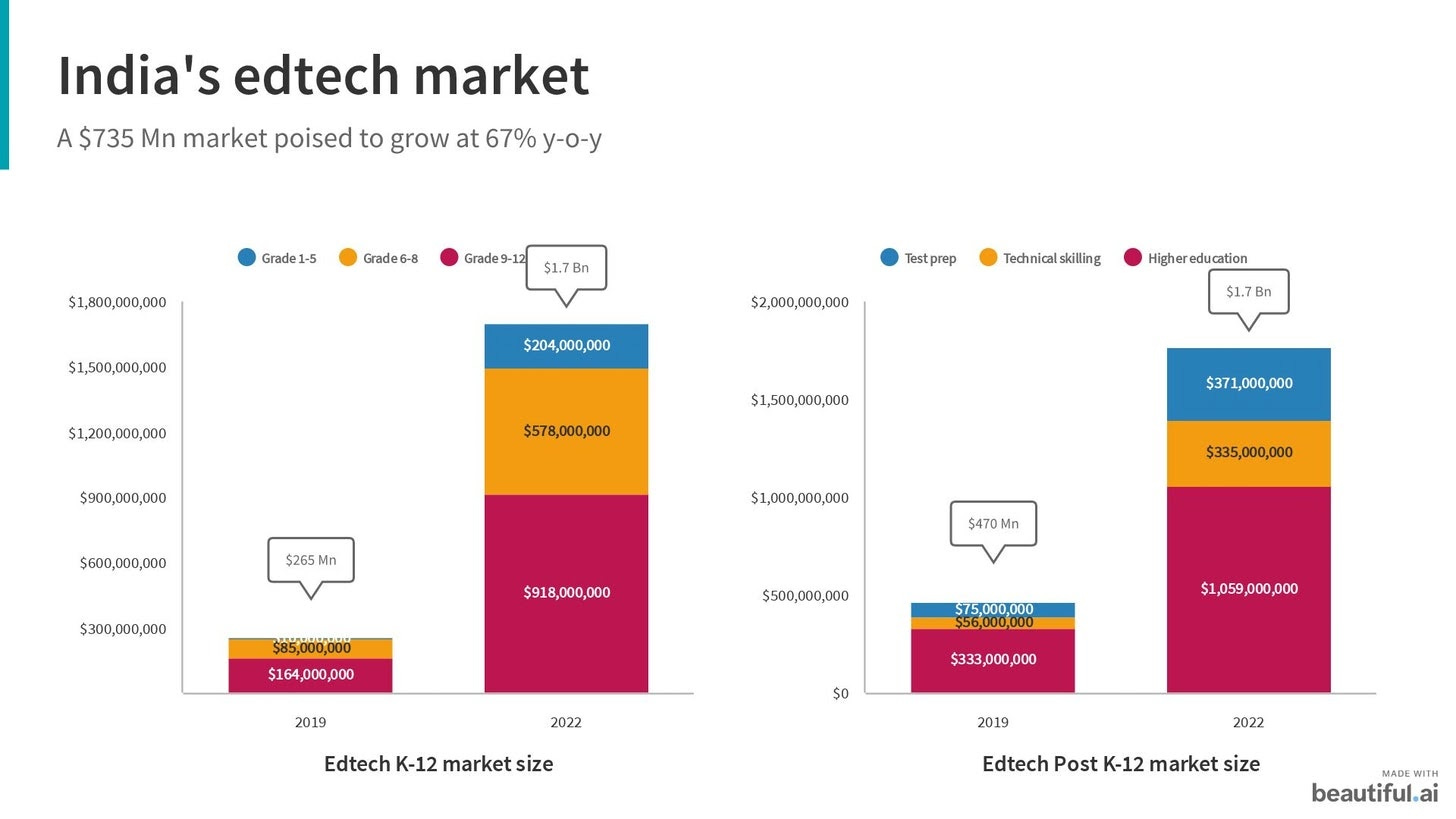

Education is amongst the top 2 spends in average households across India (versus the USA where education is 7th in spending, coming below entertainment). It’s a low volatility sector with estimated market size of $140-$150 billion in 2020. There are 275 million students enrolled in 1.5 million schools and K12 alone is a $50 billion opportunity, colleges $50 billion as well, and employment $9 billion.

The Covid tailwinds have doubled the Edtech userbase from 45 million to 90 million. With a promotion by schools and faded inertia among parents and students, the paid userbase grew from 2.5 million to 4.5 million. But with only 5% paid users, it’s still a relatively small market valuing $735 million (2019). So clearly, the money still very much lies with schools, colleges, and traditional institutes.

So once things return to normalcy, we see a clear opportunity for disruption in:

K12 hybrid learning solutions: Complementing the traditional teaching inside the classroom and empowering teachers — adapting to their role as a mentor, facilitator, and guide.

A gamified solution to learn programming in the classroom, that develops your logical thinking and problem solving, and is engaging. A teacher, in this case, is a facilitator.

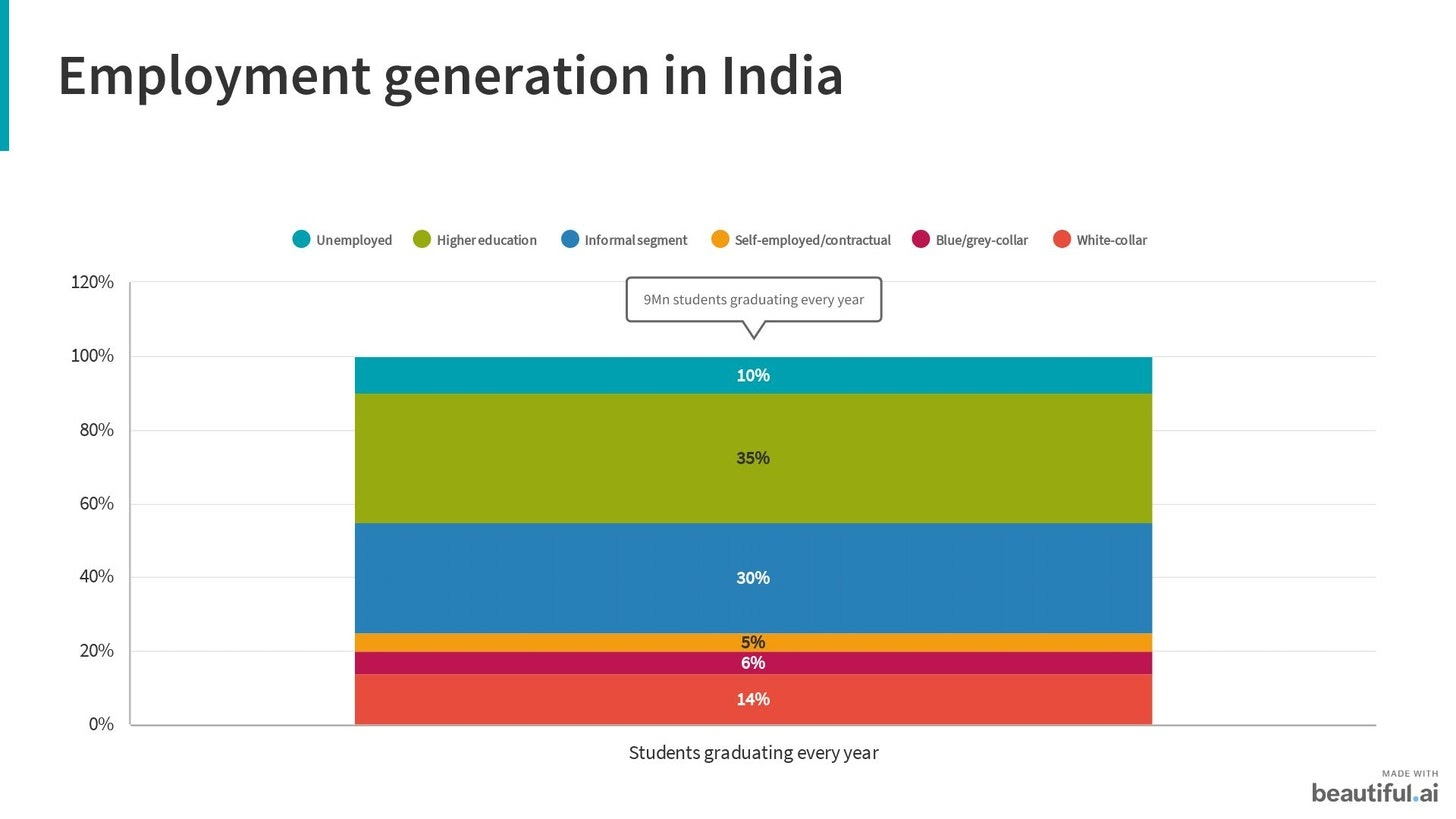

Ora product/feature that can tell teachers the list of concepts that are going wrong for particular students and needs revision — something that would benefit both teachers and students.Vocational training related solutions: Less than 7% of the Indian workforce has received vocational training. As such, 500 million Indians need to be skilled over the next 5 years, the majority being grey-collar workers, present in logistics companies, hotels, hospitals, cab and security services, receptions, sales and BPOs, IT workers, construction supervisors, and skilled technicians. The expected outcome is a professional degree/diploma followed by employment.

Much of the market we’re talking about is yet to be created since the people who are to be trained for these jobs aren’t even aware. 200 million people (40% of the total workforce) working on farms generate only 15% of our GDP. It was also one of the biggest shock absorbers of the Indian labor market due to the pandemic. Truth be told, with further mechanization and automation, we wouldn’t require a large workforce in farming. Thus, we need to aggressively upskill this population, keeping accessibility and affordability in mind.

The ISA model has successfully embedded learning outcomes in the case of software engineering programs and might work for skilling programs in healthcare, manufacturing technologies, electronics.

Another company operating in this space is Skillbee — a trusted platform for blue-grey collar workers seeking credible employment opportunities in international markets.

This points to gaps between education, skills development, and job creation where our future generations are likely to face an increasingly cut-throat workforce.

There’s little surprise that out of 4,000 Edtech startups, 37% either directly cater to K12 schools and students or offer products mapped to the curriculum.

Now while the K12 market is attractive and fairly competitive — how can Edtech provide industry-focused skills to employ grey collar India?

It’s a clear opportunity to engage and monetize the next wave of 70-100 million users. I see 2 key drivers, combined with content, technology, and service, for building a successful Edtech business here:

1. Satisfying learning outcomes with good user experience.

2. Solid customer acquisition and distribution strategy.

Can a Byju’s (or a B2C) model work in this segment?

India’s Edtech industry threw up a big surprise in 2019, with Byju’s alone taking home 54.4% of the total market. It also recently acquired WhiteHat Jr for $300 million, in one of the fastest and most remarkable exits of all time in the Indian startup ecosystem.

Just during March and April, Byju’s added 13.5 million new users. It reported $400 million in revenues in FY20. It was recently valued at $10.5 billion, 25X its revenue. Valuation for similar private companies is ~2-3X of revenue so Byju’s needs to get to $3 billion revenue to justify its valuation.

Byju’s financial metrics in FY19. Source: Entrackr. 1$ = INR 70.

So how can Byju’s get to $3 billion in revenues?

This seeded a round of debate and rightly so — because, on paper, Byju’s looks like a business with good unit economics. But for an ARPU of $77, Byju’s needs 38.5 million paid users to get to $3 billion in revenue. Even with an increased ARPU of $150, it still requires 19 million paid users. And for a $100 CAC, that means $1.9 billion - $3.8 billion spent in marketing promotion and direct sales. Those are some outrageous numbers, considering India’s online education market will be ~$3.5 billion and have ~12 million paying users by 2022.

No wonder Byju’s plans to go global (Osmo) to strengthen its bid to go public. But given the IPO market for education companies is nearly bone dry, it’s a tough task ahead for Byju’s.

What doesn’t work in B2C

High CAC

Being a B2C business in Edtech in India comes with its niggles. It’s a money guzzling business where CAC evaporates right before your eyes and there is no guarantee at the end if you have the customer or not. Byju’s spends $100 for acquiring a user — thankfully for its offerings like a $1700 subscription for 7 years, it’s LTV is pretty good even with a 15% churn. For a company to achieve scale-like Byju’s, between $10-$50 CAC, it requires a $30-$150 million upfront investment.

To be fair to Byju’s, their CAC matches the stickiness of the customer since they’re trying to get the user as early as possible (K8) to make them pay a subscription for multiple years, creating a balance between CAC and LTV by ensuring longevity.

Longer purchase cycles, trust deficit, and direct sales costs

Consumer purchases are more impulsive versus more complex education purchases, involving a lot of social information and research, making the decision cycle in matters relating to education longer. It’s hard to establish trust and display quality and results instantaneously while selling. This forces startups to balance between feet on the street and the SEO approach. Many people forget that for B2C, especially in education, there is a high likelihood of success when you do feet on the street marketing. Here is a good tale of how Byju’s pitch works.

For a sector that has long decision cycles and sticky cycles of consumer engagement, rapid transformation due to technology does seem logical post-Covid.

Personalization

B2C businesses thrive on a great level of personalization. But frankly, today, personalization is not possible. Teachers admit that they don’t know if every student understood all the concepts well and they can only assess by grading the answer scripts if a student is doing well in a subject. Outside the classroom, students are using different digital and non-digital solutions. The friction between different modes of instruction makes it difficult to truly personalize the learning experience.

B2C limits to an outside classroom environment, putting constraints on disruption (and monetization) given that students spend 50% of their daily hours at school.

Alternative models

B2B

On the flip side, one would expect building a B2B business to be far cheaper (outside of the tech) — but selling to schools and colleges is also not easy. To be fair, there isn’t any discernible difference between B2B and B2C in terms of difficulties with customer acquisition in Edtech. It’s not in line with our conventional wisdom that the cost of sales is a larger challenge for B2C Edtech businesses.

The red-tapism and bureaucracy make the sales process lengthy to persuade a school or to even pilot a product, leading to an inherently long process which is costly in terms of time and money.

There are multiple operational challenges — the school management, teachers, students, and parents are stakeholders in the products the school will use, an Edtech business must convince all decision-makers. B2B also requires the best customer-facing staff who are not only aggressive at selling but also get valuable feedback from customers and act as brand evangelists.

The enablement model

There’s a third model which we’ve seen working well, in the case of Meesho and SimSim, where you try to enable the middleman. It goes via the B2B2C route where the company sells a product/service to a business, gaining customers and/or data from that business that they get to keep and use. We have found this approach to building consumer technology businesses in India to be largely successful till yet.

How does it work?

Rakuten popularised the B2B2C model about 15 years back. It gathered all the eCommerce stores to come on Rakuten’s platform and users simply have one place to log in to shop from all these stores. Stores paid Rakuten a commission for sending users their way, and Rakuten shared the commission with users as cashback.

With that logic, any company that aggregates demand and solves the distribution problem for other companies can be B2B2C. OneCode, a referral-based distribution platform for restaurants, cosmetics, and medicine & pharmaceutical companies is a good example of a B2B2C business. Other good examples of B2B2C are Meesho (supply marketplace for resellers), SimSim (video-based eCommerce selling through micro-influencers), Wealthy (building tools for wealth advisors to manage customer experience and run their business), Classplus (tech platform for coaching teachers and institutions), and OpenTable.

The product/service you offer as a B2B2C business empowers suppliers rather than intermediating supply. For example, consider:

Amazon versus Shopify.

Unacademy versus Classplus [supply intermediation versus supply empowerment].

PS: It can be complex to differentiate between a channel partnership and a B2B2C arrangement. A channel partnership lets you acquire customers but you do not own the valuable customer data or the customer itself.

How can we employ grey-collar India operating with an enablement model?

There are 2 intermediaries underutilized in this space — teachers, and corporates.

Traditionally, teachers are more often than not commoditized on consumer platforms. Being the gatekeepers of education-related decisions, starting from needs-realization and awareness to purchase decision and experience, they provide the essential human element in Edtech to bypass leakage. A company that focuses on enabling teachers (and improving their quality), can also make teaching an attractive proposition.

A thought resonating throughout corporate and startup offices in India is the lack of employable talent. We need to partner with them to train and help them hire grey-collar talent that’s instantly deployable, based on essential skills required for each role.

As technology solutions providers, we need to bridge the gap between supply and demand which is completely skewed right now. Models that leverage teachers for trust, adoption, and engagement, can attach outcomes by becoming full-stack platforms for skilling and employment. By enabling teachers and companies with the right technology tools and platforms, these models are able to enable trust (with their reputation as collateral, the social trust inherent in offline transactions is replicated online) and enable curation.

If you think about integrating up-skilling courses with services marketplaces like Upwork — it can be a win-win. Not only does it help in creating outcomes for learning and better economics for content providers, but it can also develop a moat for the marketplace in the form of differentiated supply.

Another fine example here would be Able Jobs that is helping companies hire trained talent in sales, marketing, and operations faster, by training and vetting suitable candidates.

Why B2B2C is more suited for this

To us, the answers to improved learning outcomes are less like Netflix and more like Google Maps — starting from ascertaining where you are, where you want to go, and giving you the optimal tools to achieve the desired outcome. I say that because learning alone doesn't translate to job certainty (in the Netflix model). Job seeking has its own frictions — finding job providers, filtering tons of candidates, matching jobs with requirements, running a hiring process, etc. And perhaps, the play here is in being a job platform (Able Jobs).

Offers viable unit economics. Even though SimSim is a consumer company, we believe it mitigates the issues listed above faced by B2C companies — it maintains a low CAC by using middlemen to acquire users but owns the end-user interaction. Thus, our preference for enabling middlemen (in Tier-2+ markets) has been to leverage them as a proxy for cheaply accessing and controlling end-distribution.

B2B2C arrangement helps you diversify your revenue streams. Startups like Classplus, being B2B2C, acquire customers by enabling teachers centers to run and manage their coaching centers. Without spending much on CAC, Classplus can acquire the 70 million students who go to these coaching centers — the backbone of our education system — from tuitions to local JEE prep center to IAS coaching to other small training schools. These coaching centers have students enrolled in them from across income segments. Hence, Classplus doesn’t have to worry about acquiring these users and it still gets valuable customer data. By creating the right environment, it can create new revenue streams (on top of SaaS) by becoming a content marketplace.

What are the shortcomings of this model?

The diversity of enablers may make acquisition difficult to scale. A product that caters to various use cases for a broader range of enablers (who drive consumer adoption) finds it difficult to build a focused product offering and sales strategy.

Enablement models are usually at odds with generating network effects. It’s difficult for an enablement business to offer discoverability to end-users.

Liquidity becomes dependent on enablers’ ability to aggregate demand.

Lack of lock-in. Enablers have multiple channels for online presence and a company finds it difficult to align incentives to generate stickiness in enablers.

In conclusion

Consumer aggregators have tremendous power once they get to scale. Byju’s and a few other companies are well on their way to capturing scale amongst certain target audiences. Once they have mindshare and own the user, they can do anything – it becomes a question of building a product/service that works at that stage. The only problem is that B2C businesses are not fuel-efficient vehicles but hummers, costing a bomb in upfront investment to achieve scale. And they are fraught with maximum risk. In the case of Facebook and Amazon, a tremendous amount of effort, and staying power is required before the inflection point where you go viral compared to selling software to enterprises.

B2B(2C) businesses, in contrast, tend to offer stronger unit economics, efficacy, and operational excellence that have been long favored as the sign of a winning company.

Businesses as such, either B2C or B2B(2C), need to utilize the high willingness to pay for technical skilling that culminates in career development. We see a fundamental shift in focus to “learning for earning as an X” and think that the majority of job creation for the grey-collar segment will happen through MSMEs. Career development has certainly benefited from the ISA models, wherein a student pays only when they achieve a minimum threshold of the outcome.

Given the size of the market opportunity in India, we expect significant Edtech investments here in the future and the emergence of large scale Edtech companies. However, profitability will remain a challenge for the sector, and companies will have to continuously innovate to focus on CAC and LTV to become sustainable.

Well researched and articulated for the future growth in the ever evolving virtual learning journey involving all relevant stakeholders for impactful outcomes at all stages of Life

Impressive and we'll thought Article