Are ad-based business models practical in India?

What are some alternate approaches that can work?

Lately at work, we have been staging debates to discuss and put forth our views on our observations in the ecosystem. A few weeks back, we got down to discuss whether ad-based revenue models can be successfully monetized in India to build unicorns.

I’ve documented and condensed some of the key learnings. Let’s jump right into it.

2 kinds of business models

A consumer internet company operates either in an ad-based revenue model, or a transactional (or subscription) model, or a mix of both (many marketplaces and demand aggregators deploy a hybrid model, like Amazon, Zomato, Spotify, etc).

Ads are an income source for publishers and a medium to subsidize the price of a product for consumers. These models have thrived for decades. The internet proliferated this way of charging for your products: making them ad-supported. For the publisher, the number of logged-in users, the frequency of visits, and the timeshare started driving the ability to target and sell ads.

At the onset of the internet era, ad-supported consumer companies posed an existential threat to direct-sales companies because consumer behavior was changing — from expecting to purchase directly, to expecting someone else to purchase on their behalf. That course ran its path soon because users hate ads. Digital ads are incredibly effective in some developed digital markets but the conversion rates are quite low elsewhere.

Is advertising a sustainable model for consumer internet startups

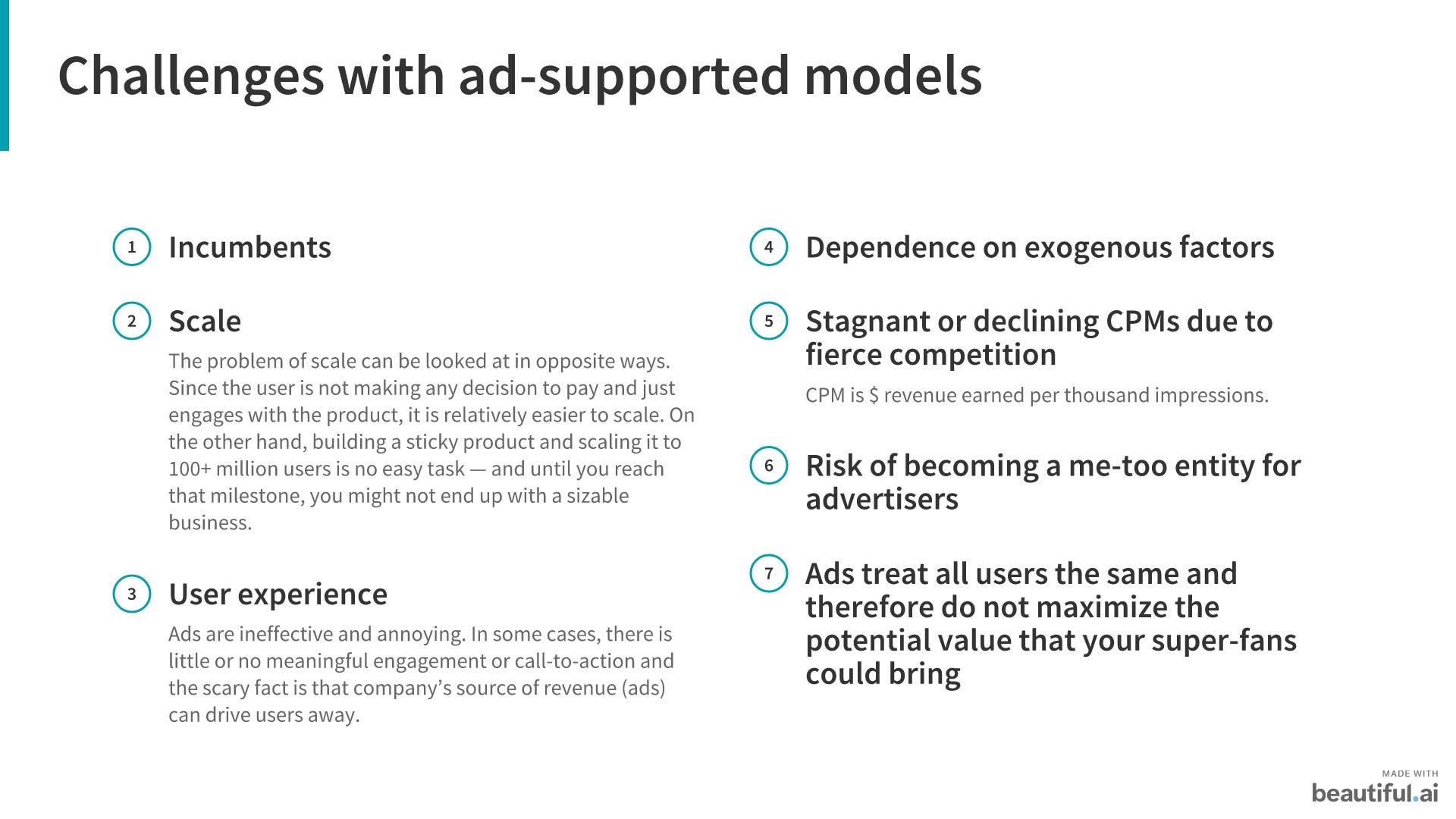

Honestly, users dislike ads, and selling ads doesn’t sound like a sexy business. In our interaction with other VCs in India, they seem a little skeptical about startups monetizing purely through ads. The concern seems justified — given the growing need for companies to create predictable revenue streams, dependence on ad revenue exposes you to market pressure where there’s little you can do as a firm.

Covid forced companies to cut back on marketing spend and subsequently the revenues tanked for the ad platforms. Such factors dictate an intrinsic unpredictability in revenues.

The total addressable market in India

Total ad-revenue in India for all mediums was $10 billion in 2019. TV accounted for $3.2 billion, print $2 billion, and digital $1.95 billion. Digital is a duopolistic market, with Facebook and Google together commanding up to 70% share followed by Linkedin, Twitter, Snapchat, Spotify, etc. Within digital, ad spend on search is $360 million, followed by video at $255 million, social media (Facebook, Linkedin, etc) at $240 million, and mobile ads at ~$250 million. Although the digital ad industry has been growing at 25% y-o-y, even at such a healthy growth rate, the overall market will remain relatively small in size ($4 billion by 2022).

In addition to the small market size, there are a host of other challenges faced in building successful ad-supported consumer internet startups.

PS: To be fair, yes the market is tiny, BUT:

Ad spends (as % of GDP) is expected to grow.

Digital is expected the eclipse print & TV very rapidly.

Digital will only become more effective due to better targeting.

A look at Inshorts

Having raised ~$30 million across 5 rounds of funding, 2 things have worked for Inshorts — the way it solves the problem of accessibility with its click-bait, short-form news, and how it uses tech. Inshorts uses AI that can condense a lengthy article into a 60-worded brief, meaning it can generate 10X more content than the competition. The idea is simple: more articles mean more time spent on the app, and thus, room to display more ads. And just like any other successful ad-supported business, it attained operational profitability rather quickly in 2017, within 3 years of inception.

Key drivers for business

Inshorts has 300 advertisers on its platform and doesn’t offer a premium subscription for its news product. Understandably so because news, entertainment (games, videos, audio), social platforms, and productivity tools are categories where users usually hate to see a paywall. The wave of subscribers who are brand champions in these categories is yet to achieve scale in India.

CTR = Click-through rate. CPC = Cost per click. CPM = $ earned per 1000 impressions.

Note: This is an estimate. Inshorts reported $10 million in revenue in 2019.

Valuation multiples for media tech companies range between 8 to 12 and Inshorts might be valued ~$100 million. That means for Inshorts to become a unicorn it would need a $100 million annual run-rate. And as you can see, Inshorts’ ARPU is pretty low ($1.5 per active user per year). For Inshorts to grow to a $100 million run-rate it would need 67 million DAUs, while sustaining its ad fill rate, CPM levels, and timeshare.

PS: it’s hard as it is to make and scale such a product, and even then, there’ll always be churn.

The problem with the eye-ball economy

I’m not suggesting that ads are bad business. After all, Google and Facebook made $205 billion in revenue last year from ads. Ad-supported companies exploit user behavior over direct sales businesses (why pay for something when advertisers are ready to subsidize it) but have their own bad economics. The problem is two-fold: it takes a well-established presence to make money from ads and ad-based models only marginally differentiate between its users.

We are also seeing a big shift taking place in marketing. The rise of social media influencers and community opinion leaders is not by accident. Influencers interact with their audiences through videos on TikTok and Instagram that creates intimacy at scale and brings authenticity in context. This is changing the way companies approach marketing and customer acquisition significantly.

Considering this, selling a product or a subscription service seems a lot more effective. But in India, entrepreneurs’ hands are tied from both ends — the Indian consumer tech market offers limited liquidity. Amongst 150 million audio listeners, less than 2 million pay, ~350 million people using OTT platforms, less than 10 million pay, 300 million people consuming news online, less than 1 million pay. You see what I’m getting at, that in India, it’s hard to sell products or subscriptions online that users can avoid paying for. Of the 550 million people online, ~100 million have ever made a purchase. Then there’s also an added layer of complexity of transaction process and trust. Unless it’s essential, willingness to pay is less. And why not? India is still a developing country with $2.5K GDP per capita, and comparisons to the US ($60K per capita) and Chinese ($10K per capita) markets are quite unfair.

Source: Entrackr.

The transition to the wallet economy

Simply put, how does a company that charges users directly for a product compete with a company that finds someone else to pay indirectly for the same product?

By focusing on user experience. Ads ruin the user experience. User loyalty comes from how companies treat their users. A consistent brand experience results in habit formation which is hard to replicate. Delivering this superior user experience has to be embedded in the DNA of the company.

The business model drives the product thinking and ad-based models focus on delivering a differentiated offering for the user that the advertiser is trying to target. The advertiser is just looking to gather eye-balls and does little to provide more utility to engaged fans. So how can companies move out of this rut and reimagine their business models?

We believe that a business model that maximizes the revenue from your super-fans and shares that value across all your customers is something worth exploring.

3 types of audience

As Shishir describes, all users can be characterized based on 2 qualities — the willingness to pay and the activation energy required for using the product. Basis these qualities, a consumer can be categorized as:

Super-fan: They pay a retail price for a product and will look for your product.

Casual-fan: They only have one of the criteria listed above.

Non-fan: Have none of the traits listed above.

If you’re solely an ad-supported business, it’s likely that you have a base of non-fan users who use your product only when necessary and have little or no loyalty. Instead, when you charge your users, it’s a validation of your value to your super-fans that stick to your platform and do repeat purchases.

The super-fans want more utility, connection, status within the platform, and are willing to pay a rate above the ads. And best of all super-fans are willing to spend money and will be extremely satisfied with their purchase if the user experience is good. Super-fans are actually glad they pay significantly more than the casual-fans. The question is what’s the best way to monetize your super-fans?

Zomato’s super-fan strategy

Zomato is a good example of a company trying to enable super-fan behavior amongst its users with their Zomato Gold (now Zomato Pro) subscription.

For a good time since starting operations, Zomato depended on ad revenue through featured listings. But it offered limited scale and growth and Zomato’s ad revenue became stagnant between $35-$45 million. In response, it chose to not only add the layer of transaction but also to create a super-fan user base and maximize the revenue from them. Zomato’s aggressive expansion in the food delivery business generated $350 million in revenue in FY20, a 2.4X growth from $150 million in FY19. The transactional layer boosts featured listings since Zomato services 2 million orders/day and restaurants want to ride this wave of demand. It also improves the quality and intent of the audience, which is a rarity in ad-supported models.

The introduction of Zomato Gold set the flywheel rolling and created network effects — repeated purchases meant more purchasing power for Zomato and thus better pricing for all users. With ~1 million Gold subscribers, it adds $15 million in ARR and presents an opportunity to take a cut off of every transaction for payments.

What Zomato did lose in the process was EBITDA profitability, burning $20+ million every month in FY20 but seems to be on track for an IPO next year.

Other ways to monetize super-fans

What we’ve seen working well in the Indian scenario is charging for featured listings in a hybrid model, instead of pure ads. Zomato, Swiggy, Quikr, OLX have been successful in harnessing this revenue stream more efficiently compared to competing non-transactional consumer internet companies. These companies, most importantly, can predict consumer behavior and demand more accurately using the historical transactional data which translates into a sustainable advantage. But these companies have the advantage of enabling direct sales through their marketplace. What can consumer product companies possibly do to monetize their super-fans successfully?

Bundling and subscriptions

One option is to become a part of a bundle. PayTM First for instance. Airtel bundles different content offerings with its telecom service (Amazon Prime, Hotstar, etc). Bundling helps in product distribution and overcoming the barrier of customer conversion since users view bundles as value for money deals. It helps convert some of your casual-fans into super-fans and offers more value to your super-fans.

Micro-purchases

We can also learn from the Chinese consumer internet companies and how they evolved their business models. Apps in China are enabling micro-purchases (small value items like buying a book chapter by chapter for example) to start slow and build a behavior. Once a user is comfortable paying on the platform, he or she is more likely to upgrade to premium offerings. In-app micro-purchases (or tipping) can be useful in assessing a user’s willingness to pay as well. Tencent’s WeChat is monetizing group-chats by enabling conversational commerce of services like tourism.

Personalized subscriptions, bundling, and in-app purchases can unlock the true impact and value of super-fans that creates shared value for all users.

In conclusion

For any consumer internet company, it depends on what they envision to achieve in the future. Nothing is off-limits for incumbents and it is inevitable to avoid competition. In the war to grab our eye-balls and our wallets, the key instrument for a company will be the business model that it adopts.

I think the moat for any consumer internet company is aggregation. Once consumers are aggregated, they can be monetized in many different ways (even if it's not ads that are most effective). That’s exactly what Cred is doing — creating a gated community of high-trust individuals and the business models can be added on top later.

Standalone ad businesses in India do not seem ideal for venture capital because the market is small and heavily crowded. The growth too is seeming to slacken, even for the giants like Google and Facebook.

Given that, I believe that hybrid models with a focus on monetizing super-fans will be the most effective choice in command.